IMPORTANT: On December 19, 2025, New York Governor Kathy Hochul vetoed Senate Bill 8432, a proposed amendment to the New York Limited Liability Company Transparency Act (NY LLC Transparency Act) that would have broadened its scope.

In her message, Hochul explained that imposing requirements beyond what the federal law mandates was not in the state’s interest and would create additional burdens on businesses.

The practical result of the recent veto? When the NY LLC Transparency Act takes effect on January 1, 2026, it will remain tied to the federal definitions and therefore will apply only to LLCs formed outside the United States that are registered to do business in New York. Domestic LLCs are exempt.

What The Recent Veto Means for LLCs:

Foreign LLCs registered in New York must still file BOI reports with the New York Department of State — generally within 30 days of authorization to do business, or by January 1, 2027 for existing registrations.

Domestic LLCs: No state filing requirement under the NY LLC Transparency Act at this time.

In summary, the veto means that New York aligns its LLC reporting scope with the narrowed federal framework, meaning most U.S.-organized LLCs remain exempt from state-level reporting — for now.

We will continue sharing updates if/when the reporting mandate evolves or changes.

Filing deadlines depend on when the LLC was formed or registered.

LLCs Formed or Registered Before January 1, 2026

Initial BOI report or exemption attestation due by January 1, 2027

LLCs Formed or Registered On or After January 1, 2026

Initial filing due within 30 days of formation or registration

After the initial filing, all LLCs must file annually.

Who Has to File a BOI Report in New York?

The Core Rule

An entity must file under New York’s BOI rules if it is:

A New York domestic LLC, or

A foreign LLC authorized to do business in New York

These entities are collectively considered LLCs “formed or registered to do business in New York.”

Each such LLC must file one of the following:

A BOI report, or

An attestation of exemption

Reporting LLC vs Exempt LLC

Which LLCs Must File a BOI Report?

An LLC must file a BOI report if it does not qualify for an exemption under the NYLTA.

Reporting LLCs must:

File an initial BOI report, and

Submit an annual statement confirming or updating ownership information

Which LLCs Are Exempt?

New York recognizes the same general exemption categories used under the federal CTA, including:

Large operating companies

Banks and financial institutions

Public companies

Insurance companies

Registered investment advisers

Certain nonprofit entities

Subsidiaries of exempt companies

Important: Exempt LLCs are still required to file.

Instead of a BOI report, exempt LLCs must file an attestation of exemption stating:

Which exemption applies

Facts supporting the exemption

A certification signed under penalty of perjury

Exempt LLCs must also confirm their exemption annually.

What Is a Beneficial Owner Under New York BOI Rules?

For reporting LLCs, a beneficial owner is any individual who:

Owns or controls 25 percent or more of the LLC, or

Exercises substantial control over the LLC

Substantial control includes:

Senior officers

Individuals with authority over major decisions

Persons with appointment or removal power

There is no cap on the number of beneficial owners that must be reported.

Who Is an Applicant?

New York also requires disclosure of LLC applicants.

An applicant generally includes:

The person who files the formation or registration documents, and

Any individual who directs or controls that filing

This commonly includes law firm staff, paralegals, registered agent services, or internal employees.

Unlike federal BOI rules, New York requires applicant information even for LLCs formed before 2026.

What Information Is Required in a New York BOI Filing?

For Reporting LLCs

Legal name and principal office address

Jurisdiction of formation

NYDOS identifiers

Beneficial owner information:

Full legal name

Date of birth

Address

Government-issued ID number

For Applicants

Same personal information as beneficial owners

New York does not provide a reusable ID system. Information must be submitted for each filing.

For Exempt LLCs

Exemption category

Supporting facts

Annual confirmation

Is New York BOI Information Public?

No. BOI data is stored in a secure NYDOS database and is not publicly accessible.

However, compliance status is public. LLCs that fail to file can be labeled “Past Due” or “Delinquent,” which may be visible to banks, investors, and counterparties.

What Are the Penalties for Not Filing?

Failure to file can result in:

Public noncompliance status

Civil penalties of up to $500 per day

Potential suspension, dissolution, or loss of authority to do business in New York

For companies managing many LLCs, penalties can accumulate rapidly.

Summary: Do You Have to File a BOI Report With New York?

If an entity is an LLC formed in New York or registered to do business in New York, it must file something under the New York LLC Transparency Act.

Reporting LLCs file BOI reports

Exempt LLCs file exemption attestations

All covered LLCs file annually

For high-volume LLC filers, New York BOI compliance is not optional and not one-time.

It is an ongoing, portfolio-wide obligation that requires structured tracking and repeatable processes.

IMPORTANT UPDATE: Please refer to our most recent post for the newest information on the New York LLC Transparency Act HERE.

If you operate an LLC in New York, one of the most common questions right now is simple but critical: Am I exempt from NY BOI reporting?

The answer is often misunderstood.

Even if your LLC qualifies for an exemption, you are still required to file with New York.

There is no “do nothing” option under New York’s Beneficial Ownership rules.

Below is a clear, practical breakdown of who is exempt, what exemption actually means in New York, and what exempt LLCs are still required to file.

Important Legislative Context (December 2025)

As of mid-December 2025, there is pending legislation that could affect the final scope of NY BOI reporting. Governor Hochul has until December 19, 2025 to act on Senate Bill S8432, which would clarify that NYLTA applies broadly to both domestic and foreign LLCs.

This article assumes the bill is signed and the full exemption framework applies. LLCs should continue monitoring New York Department of State guidance for updates.

Who Is Covered by NY BOI Rules?

Before asking whether you are exempt, you need to confirm whether your entity is in scope.

You are covered by NY BOI rules if your entity is:

A New York LLC (formed by filing Articles of Organization with NYDOS), or

A foreign LLC (formed elsewhere but registered to do business in New York)

If your entity is an LLC and touches New York, you must file either:

A BOI report, or

An attestation of exemption

The 23 Exemptions New York Recognizes

New York adopted the same 23 exemption categories used in the federal Corporate Transparency Act. However, New York applies them differently.

Below is a structured overview of those exemptions.

Financial Institutions and SEC-Regulated Entities

These entities are generally exempt because they are already subject to extensive federal or state oversight.

Common exemptions include:

Public companies reporting under the Securities Exchange Act

Federal, state, local, or tribal government entities

Banks and bank holding companies

Credit unions

SEC-registered broker-dealers

Securities exchanges and clearing agencies

Registered money services businesses

These exemptions typically apply to large, heavily regulated organizations, not small operating LLCs.

Investment and Fund-Related Exemptions

Certain investment structures qualify for exemptions, including:

SEC-registered investment companies

SEC-registered investment advisers

Venture capital fund advisers that file Form ADV

Certain pooled investment vehicles advised by regulated entities

Important limitation: subsidiaries of pooled investment vehicles are not exempt unless they meet separate criteria.

Insurance and Other Regulated Businesses

New York recognizes exemptions for:

Insurance companies

State-licensed insurance producers with a physical U.S. office

Public accounting firms registered under Sarbanes-Oxley

Regulated public utilities

Certain financial market utilities

Again, these exemptions generally apply to regulated operating entities, not holding companies.

Tax-Exempt and Nonprofit Organizations

Entities that qualify under the Internal Revenue Code may be exempt, including:

501(c) tax-exempt organizations

Certain political organizations

Charitable trusts under Section 4947

Important clarification:

Losing 501(c) status triggers a 180-day grace period

“Nonprofit” in name alone does not qualify. IRS status controls.

Entities that exist solely to support tax-exempt organizations may also qualify, but the ownership and funding requirements are strict.

Operating Company Exemptions (Most Common, Most Misunderstood)

Large Operating Company Exemption

This exemption applies only if all three conditions are met:

More than 20 full-time U.S. employees

More than $5 million in U.S. gross receipts on the prior tax return

A physical operating office in the United States

Most small businesses and holding LLCs do not qualify.

Subsidiary of an Exempt Entity

An LLC may be exempt if it is:

100% owned or 100% controlled by certain exempt entities

Partial ownership does not qualify. FinCEN and New York interpret “controlled” strictly.

Inactive Entity Exemption

This exemption is extremely narrow. To qualify, an LLC must meet all six criteria:

Existed before January 1, 2020

No active business operations

No foreign ownership

No ownership changes in the last 12 months

Less than $1,000 in financial activity

No assets anywhere

Very few entities qualify.

What Most LLCs Get Wrong About Exemptions

Common misconceptions include:

Being unprofitable does not create an exemption

Single-member LLCs are not exempt

Real estate holding LLCs are not exempt

Passive income does not qualify as inactivity

HOAs not classified under 501(c) are not exempt

For most small businesses and real estate LLCs, BOI reporting is required.

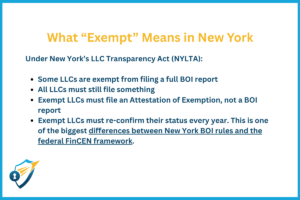

What Exempt LLCs Must Still File

This is the critical New York difference.

Even if your LLC is exempt, you must file:

An Attestation of Exemption

This filing must include:

The specific exemption claimed

Facts supporting the exemption

A certification signed under penalty of perjury

Annual Confirmation

Every exempt LLC must also file an annual statement confirming the exemption still applies.

Federal rules do not require this. New York does.

Filing Deadlines for Exempt LLCs

LLCs existing before January 1, 2026: file by January 1, 2027

LLCs formed or registered after January 1, 2026: file within 30 days

Missing deadlines triggers the same penalties as non-exempt entities.

Penalties for Not Filing

Failure to file an exemption attestation can result in:

Public “past due” status after 30 days

“Delinquent” status after two years

Fines up to $500 per day

Possible suspension or dissolution by the Attorney General

Exempt status does not reduce enforcement risk.

Bottom Line: Am I Exempt From NY BOI Reporting?

Here is the simplest way to think about it:

If your entity is an LLC in New York, you must file

Exempt LLCs file an attestation, not a BOI report

Non-exempt LLCs file a full BOI report

Everyone files annually

If you manage or form LLCs at scale, exemption analysis is going to be a recurring compliance workflow.

IMPORTANT UPDATE: Please refer to our most recent post for the newest information on the New York LLC Transparency Act HERE.

If you operate or manage LLCs in New York, one of the most confusing compliance questions right now is this: What is the difference between NY BOI reporting and the federal CTA (Corporate Transparency Act)?

The short answer is that they are no longer aligned.

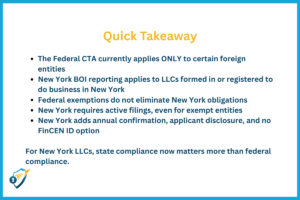

While the federal CTA has narrowed dramatically, New York has moved in the opposite direction by creating an independent, state-level reporting regime that applies to LLCs, regardless of federal status.

Below is a clear breakdown of how the two systems differ, why federal exemptions do not protect New York LLCs, and what that means in practice.

Scope and Applicability

Federal Corporate Transparency Act (Current Status)

When the CTA was enacted, it applied broadly to domestic corporations, LLCs, and similar entities. That changed in March 2025.

Under FinCEN’s interim final rule:

Domestic U.S. entities are exempt

Only foreign entities registered to do business in the U.S. must report

Federal BOI reporting is effectively paused for most U.S. companies

This is a major contraction of federal scope.

New York LLC Transparency Act

New York did not follow this narrowing.

Under NYLTA:

Applies only to LLCs

Covers:

New York–formed LLCs

Foreign LLCs authorized to do business in New York

Does not apply to corporations or LPs

Becomes effective January 1, 2026

Even if an LLC is fully exempt under the federal CTA, it may still be fully reportable in New York.

Core Difference: Federal Retreat vs. State Expansion

The most important distinction is structural.

The federal system pulled back

New York doubled down

As a result, New York LLCs cannot rely on federal exemption status to avoid state compliance.

Beneficial Owner Definitions

On this point, the two laws are aligned.

Both define a beneficial owner as an individual who:

Owns or controls 25% or more of ownership interests, or

Exercises substantial control over the entity

There is no meaningful difference in how beneficial owners are identified. The divergence begins after identification.

Reporting Requirements and Data Collection

What Both Require

Both regimes collect:

Full legal name

Date of birth

Residential or business address

Government-issued ID number

Where New York Goes Further

New York imposes additional burdens not present in the current federal framework.

Applicant Disclosure

Federal CTA: required only for entities formed on or after January 1, 2024

New York: required for all LLCs, including those formed years ago

FinCEN Identifier

Federal CTA: allows use of a FinCEN ID to avoid re-entering personal data

New York: no equivalent exists

Every filing requires full personal data again.

Document Submission

Federal CTA: requires copies of ID documents

New York: does not require document uploads but requires more frequent filings

Exemptions: Same Categories, Very Different Behavior

Both laws recognize the same 23 exemption categories, including:

Banks

Public companies

Large operating companies

Certain nonprofits

Regulated financial entities

The difference is what happens next.

Federal CTA Exemptions

Under the CTA:

If you are exempt, you do nothing

No filing

No confirmation

No renewal

Exemptions are self-executing.

New York Exemptions

Under NYLTA:

Exempt LLCs must file

They must submit an Attestation of Exemption

The attestation must:

Identify the exemption

Provide supporting facts

Be signed under penalty of perjury

New York converts exemption into an active compliance obligation.

Annual Filing Requirement

This is another major divergence.

Federal CTA: event-based updates only

New York: mandatory annual confirmation

Every LLC must file annually:

Reporting LLCs confirm or update BOI

Exempt LLCs confirm exemption status

There is no equivalent annual requirement under federal law.

Filing Deadlines

Federal CTA (Current)

Domestic entities: no filing required

Foreign entities: 30 days from U.S. registration

Updates: within 30 days of changes

New York LLC Transparency Act

Existing LLCs: file by January 1, 2027

New LLCs (post-2026): file within 30 days

All LLCs: annual filing required

New York’s calendar-style compliance is broader and more predictable, but also more burdensome.

Confidentiality and Public Access

Both systems now protect BOI data from public disclosure.

Federal: non-public FinCEN database

New York: non-public NYDOS database

However, New York publicly displays compliance status.

LLCs that miss deadlines may be marked:

“Past Due”

“Delinquent”

This visibility can affect banking, contracts, and transactions.

Penalties and Enforcement

Federal CTA

Civil penalties: up to $500 per day

Criminal penalties for willful violations

Enforced by FinCEN and DOJ

New York

“Past due” status after 30 days

“Delinquent” after two years

$250 initial penalty

Up to $500 per day ongoing

Possible suspension or dissolution by Attorney General

New York penalties are civil and administrative, but the operational risk is significant.

Legislative Uncertainty Still Matters

As of December 2025, New York lawmakers have acted to preserve state-level reporting regardless of federal changes. Pending legislation would confirm that NYLTA applies to both domestic and foreign LLCs.

The intent is clear: New York does not plan to follow federal retrenchment.

Practical Compliance Reality

For New York LLCs:

Federal exemption does not remove state obligations

Exempt entities still file annually

Applicant data must be tracked long-term

No FinCEN ID shortcut exists

For foreign LLCs in New York:

Dual compliance may apply

Separate systems and timelines must be managed

The Bottom Line

The difference between NY BOI reporting and the federal CTA is not technical. It is structural.

Where the federal BOI is currently narrow and limited, the New York BOI is broad, active, and recurring. Exemptions reduce data disclosure, not filing obligations, and annual compliance is unavoidable for New York LLCs.

If you manage LLCs connected to New York, state compliance now carries more weight than federal compliance, and planning around that reality is no longer optional.

IMPORTANT UPDATE: Please refer to our most recent post for the newest information on the New York LLC Transparency Act HERE.

Let’s cut to the chase. Before diving into the details, here’s what you need to know now:

Now, let’s explore the nitty-gritty details, as they are crucial if you or your clients belong to the “Who” category mentioned above.

What is the New York LLC Transparency Act, Really?

The New York LLC Transparency Act (NYLTA), effective January 1, 2026, establishes state-level beneficial ownership reporting requirements that mirror many aspects of the federal Corporate Transparency Act, imposing new disclosure requirements on LLCs formed or registered to operate in New York.

Filing Deadlines

For existing LLCs (formed or authorized before January 1, 2026), the initial BOI report or attestation of exemption must be filed by January 1, 2027.

For new LLCs (formed or authorized on or after January 1, 2026), the filing must be submitted within 30 days of formation or registration.

After the initial filing, all LLCs must submit an annual statement confirming or updating their beneficial ownership information, principal executive office address, and exemption status.

Who Has to Report?

Any individual (considered a “beneficial owner”) who meets either of these criteria:

Owns or controls at least 25% or more of the LLC’s ownership interests

Exercises substantial control over the LLC

The law applies to all LLCs except those that qualify for one of 23 exemptions that mirror the federal Corporate Transparency Act.

A few key exemptions include large operating companies (with more than 20 full-time U.S. employees, gross receipts of $5 million or more, and a physical office in New York), publicly traded companies, banks and credit unions, tax-exempt entities, and investment companies.

Important Note: Even exempt LLCs must file an annual attestation of exemption under penalty of perjury indicating which exemption applies. In other words, every LLC has to file something.

What Information is Required?

Each beneficial owner must provide:

Full legal name

Date of birth

Current home or business street address

A unique identifying number from an acceptable ID (U.S. driver’s license or passport)

What Are the Penalties for Non-Compliance?

Similar to FinCEN’s former federal reporting requirements, the consequences for failing to file or update your NY reports/ attestations of exemption are steep, increasing in intensity as time goes on.

After 30 Days: Entity is marked “past due” in state records.

After 2 Years: Entity is given a “delinquency” status in state records; requires filing a corrected report plus a $250 penalty to remove the status, along with daily fines.

Ongoing Penalties: Up to $500 per day for failure to file or update. In extreme cases of non-compliance, the Attorney General may suspend or even dissolve the LLC.

How is the New York LLC Transparency Act Different From the CTA?

The NY LLCTA has a few important distinctions:

Annual statement requirement: All New York LLCs (exempt or not) must file an annual statement to confirm or amend information submitted previously.

Private database: Information is maintained confidentially by the New York Department of State, not publicly accessible.

Applicant information: The NYLTA only requires beneficial owner information, not company applicant information.

No FinCEN ID equivalent: Unlike the CTA, beneficial owners and applicants will be required to submit their personal information.

How Can LLCs File?

All BOI reports and attestations of exemption must be filed electronically with the New York Department of State in the form and manner they prescribe.

What Can LLCs Do Now?

Stay on top of updates! One great way to do this is by following Secure Compliance on LinkedIn or bookmarking our website on your browser. We’re staying informed as policies are developed, and our content will be regularly updated to share what we’ve learned.